Leaders aren’t simply coping with regulations, and technology shifts, they’re additionally getting ready Mining pool for a future where belief and genuine buyer connection will matter greater than ever. At the identical time, they have to keep pace with fast technological developments, navigate intensifying competition, and adapt to ever-evolving buyer demands. 61% of establishments place GenAI amongst their prime funding priorities, and 57% view it as critical to long‑term relevance. Adoption is most superior in cybersecurity and fraud, where more than 80% have energetic pilots or stay use instances, and greater than 90% report comparable progress in fraud detection. IoT devices also improve the consumer expertise by providing customized and context-aware providers. For occasion, a sensible fridge might mechanically reorder groceries when provides run low, and the cost could be processed seamlessly in the background.

While overall development remains robust, growth is slowing as markets mature and adoption broadens. Aggressive benefit more and more is determined by margin management, fraud prevention, and differentiated buyer experience quite than scale alone. Payments are evolving, and businesses that keep ahead of those developments may have the advantage.

- As new applied sciences turn into more commonplace, banks and fee service suppliers (PSPs) must leverage them to streamline operations, drive business development, and innovate their product and repair offerings.

- Social media integration further personalizes client experiences, resulting in larger loyalty and elevated transaction volumes.

- Common audits, workers training, and real-time compliance monitoring are crucial to defend against cyber threats while meeting standards like PCI-DSS and GDPR.

Open Day Executive Mba Case Research: Amazon Go – Iese Enterprise College

In a world the place business strikes at digital velocity, having cost infrastructure that may keep pace isn’t just a bonus; it’s important for survival. Establishments are sharpening the expertise throughout online (96%) and cellular (95%) channels, and investing in messaging, chat, and virtual assistants to chop friction for everyday tasks. Half of leaders see modernizing digital channels as essential to delivering better, more personalised service, with 52% pushing to evolve and compete more successfully with fintechs. Anticipate 2026 to emphasize fewer steps, sooner steerage, and consistency across devices—the hallmarks of an easier, more reliable relationship with your bank. With consistent, structured remittance information and clearer beneficiary data, payments are much less prone to be delayed, flagged or rerouted. Straight-through processing improves, reconciliation turns into faster and exception handling declines.

Progress Of Digital Wallets

Moreover, person interface complexities, transaction failures, and difficulties getting refunds or resolving disputes have negatively impacted client confidence 49. Belief just isn’t only concerning the safety of funds but in addition in regards to the reliability and responsiveness of the service 50. In addition, users may also be concerned about the privateness and data safety of their personal info when using cell wallets. Additionally, the shortage of standardised rules and guidelines for cellular pockets suppliers can further contribute to consumer distrust and uncertainty 50. India’s telecom infrastructure has increased, with widespread 4G connectivity and an ongoing transition to 5G networks.

They significantly cut back cart abandonment charges — from over 70% for multi-step checkouts to under 1% for one-click experiences. For example, at Noda, we offer an option to save tons of bank details, making 1-click checkout attainable for EU and UK prospects. One Other important trend is the growing demand for cross-border B2B funds in real-time as business transactions don’t stay contained to 1 nation or location. Accordingly, corporations able to developing profitable, streamlined, low-cost solutions to cross-border transactions have a possibility to access this new and increasing income channel.

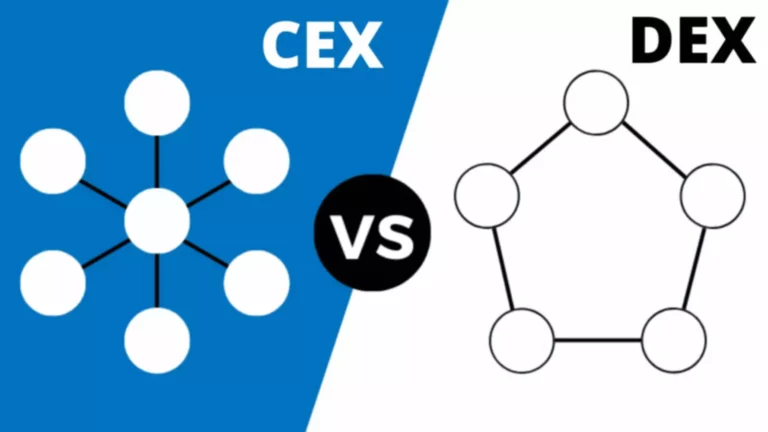

Decentralized Finance (defi) Infrastructure

The Internet of Things (IoT) is expanding the cost acceptance community to incorporate a variety of connected gadgets. From good house gadgets to related vehicles and wearables, IoT is enabling new forms of commerce. For instance, consumers can now make funds through their smartwatches or even their fridges.

The new ISO messaging commonplace will deliver order to a disjointed funds panorama, however banks must be ready. Notably, all payments suppliers are starting to acknowledge the potential of digital belongings, cryptocurrencies and DLT know-how to help improve and rework clearing and settlement processes. The adoption of real-time rails unlocks super innovation throughout overlay providers, enabling all PSPs to serve prospects better by way of A2A, which is further reinforced and accelerated by open banking. Open banking has created a new financial institution fee technique and a framework for payments innovation. Though it doesn’t present a brand new set of payment rails, open banking creates a model new mechanism for fee initiation, in effect, open funds.

This isn’t simply technological progress; it’s a elementary reimagining of how money strikes throughout borders in our interconnected world. Key challenges embody legacy system integration, data privateness & compliance, talent gaps, resistance to change https://www.xcritical.in/, value of innovation, and managing complexity during scaling. Serving To purchasers meet their business challenges begins with an in-depth understanding of the industries by which they work.

Is Financial Aid Available?

Comparative studies across various cultural and socio-economic backgrounds may additional enrich our understanding of the multi-faceted nature of cellular cost adoption in India. Total, a multidisciplinary and holistic method to analysis is crucial to comprehensively perceive and handle the complexities of mobile payment adoption in India. Firstly, it goals to comprehensively analyse the present state of cellular payment systems in India, tracing their evolution, current usage patterns, and the components driving their development 15.

The APAC region digital payment technologies has witnessed the most important adoption of digital wallets and super apps in comparability with North America and Europe, which are nonetheless closely reliant on payment cards and card networks. As of the present, India’s cellular cost landscape is characterised by speedy growth and widespread acceptance. The volume and value of transactions performed via mobile cost methods have been constantly breaking information. UPI, specifically, has seen an exponential enhance in user base and transaction volume, indicating a growing desire for this mode of cost over traditional strategies 11, 26.